Substantially revised and updated on May 15, 2016.

On Thursday, May 12, the Finance Committee of the Riksdag had a hearing on the review by Marvin Goodfriend and Mervyn King of Swedish monetary policy. I had the opportunity of asking some questions at the hearing. They were:

My questions

The review says that the interest-rates hikes 2010-11 were not unreasonable in the light of all the available information at the time. But unemployment in 2010 was very high and was peaking at 9 percent. The Riksbank’s own unemployment forecast was far above the Riksbank’s estimate of the long-run sustainable unemployment rate. And its inflation forecast was below the inflation target. Why would it be reasonable to tighten monetary policy, increasing the interest rate, in that situation? This would lead to unemployment further above the long-run sustainable rate and inflation further below the target. This implies worse target achievement, which is exactly what later happened. Instead, in such a situation, monetary policy should instead be more expansionary, to improve target achievement.

In this context, the review says that the minority only wanted a slightly lower interest rate and interest-rate path than the majority. But the minority actually followed a very simple and robust policy rule, “handlingsregel” in Swedish: As long as the inflation forecast is below the inflation target and the unemployment forecast is above the long-run sustainable unemployment rate, the interest rate and the interest-rate path should be lowered, one step at each policy meeting, to eventually get to a “well-balanced” policy. Because the starting point was far from a well-balanced policy, several steps and meetings would be needed. The lower interest rate and interest-rate path of the minority was thus just the first step of several, not the only step.

Why did the reviewers not report and discuss this simple and robust policy rule, especially since it appears so clearly from the minutes and speeches at the time, in 2010?

More generally, why is there no discussion in the review of the principles of flexible inflation targeting, what is meant by a well-balanced policy, and what policy rules are appropriate to achieve a well-balanced policy? One would think that that should be a necessary part of a review of Swedish monetary policy.

And, finally, why does the review not mention and discuss the important fact that, already in 2010, there was a substantial amount of empirical research that all implied that the costs of leaning against the wind exceeded the benefits? For instance, in a speech in November 2010 (footnote 2), I mentioned more than half a dozen of papers with this implication.

King’s (misleading) reply

Goodfriend and King did not reply to the specific questions I asked (what could they have said?). Instead, Mervyn said to me (approximately, from my memory and the Riksdag’s soundtrack of the simultaneous interpretation into Swedish):

You cannot rewrite history. In April 2011, not only were you ready to vote for a policy rate very close to the majority’s rate. You also argued that the policy rate should continue to rise, not fall, which is what you should have said given what you said now. You said that the policy rate should continue to rise and to reach 3.9 percent early 2014, a policy rate that was even higher than what the majority proposed. You cannot say that you were not in favor of higher policy rates at that time.

My response

I did not get an opportunity to respond to this at the hearing. Instead, my response is here:

What King said is obviously intended to give the impression that I thought that the appropriate and well-balanced policy in April 2011 was a rising policy rate very close to the majority’s policy rate. What he said is also intended to give the impression that my vote in Aprils 2011 was inconsistent with the policy rule I mentioned earlier.

King and the review try to give the impression that I thought that the appropriate and well-balance policy was very close to the majority’s policy, and thus that the majority’s policy 2010-2011 “was broadly accepted by all members” (a statement that is bizarre, as demonstrated here, for instance).

That impression King and the review try to give is wrong. King gives the wrong impression of my position by leaving out several things, things that he must know if he has read the minutes from the policy meetings.

Furthermore, if King had read my speeches at the time, he would have seen that these issues are discussed in detail in a May 2010 speech of mine. (It is clear from the misunderstandings in the review that Goodfriend and King have not read any of my speeches.) [Added on May 23]

King leaves out that the minority’s policy rate and policy-rate path that I voted for was a shift down compared to the majority’s rate and path. He leaves out the crucial aspect that the minority’s path was substantially more expansionary than the majority’s path. He leaves out that the minority’s path was nevertheless only the first step toward an appropriate and “well balanced” policy. It was not the only step required to reach such a policy. He leaves out that a more expansionary policy-rate path will trivially tend to lead to a higher policy rate at the end of the forecast horizon, for the simple reason that a more expansionary path makes the economy strengthen more rapidly and therefore later on justifies a higher policy rate. Altogether, he leaves out that my vote in April 2011 was fully consistent with the policy rule I mentioned earlier.

To repeat, the policy rule is that, if the inflation forecast is below the inflation target and the unemployment forecast is above the long-run sustainable rate, monetary policy should be more expansionary, and the policy rate and the policy-rate path should be lowered, that is, shifted down, one step. This would bring the inflation forecast up closer to the inflation target and the unemployment forecast down closer to the long-run sustainable rate and therefor improve target achievement.

At the next meeting, if the inflation forecast would still be below the inflation target and the unemployment forecast would still be above the long-run sustainable rate, the policy-rate and policy-rate path should again be shifted down one step.

This would then continue at each meeting until (1) either the unemployment forecast would be below the long-run sustainable rate or the inflation forecast would be above the inflation target and (2) the two forecasts together provide sufficiently good target achievement. Here target achievement is measured by how close the inflation forecast is to the target and how close the unemployment forecast is to the long-run sustainable rate during the forecast period. If required, target achievement can be measured by mean squared gaps, as I explained several times in the minutes and speeches, especially this.

In theory, one should be able to compute the size of the one large step down so as to reach the appropriate and well-balanced policy in one single step. In practice, technical limitations of Riksbank analysis prevented this. Furthermore, a large surprise of the market would not have been appropriate. Most importantly, taking a several moderate steps down is a much more robust policy with less information requirements.

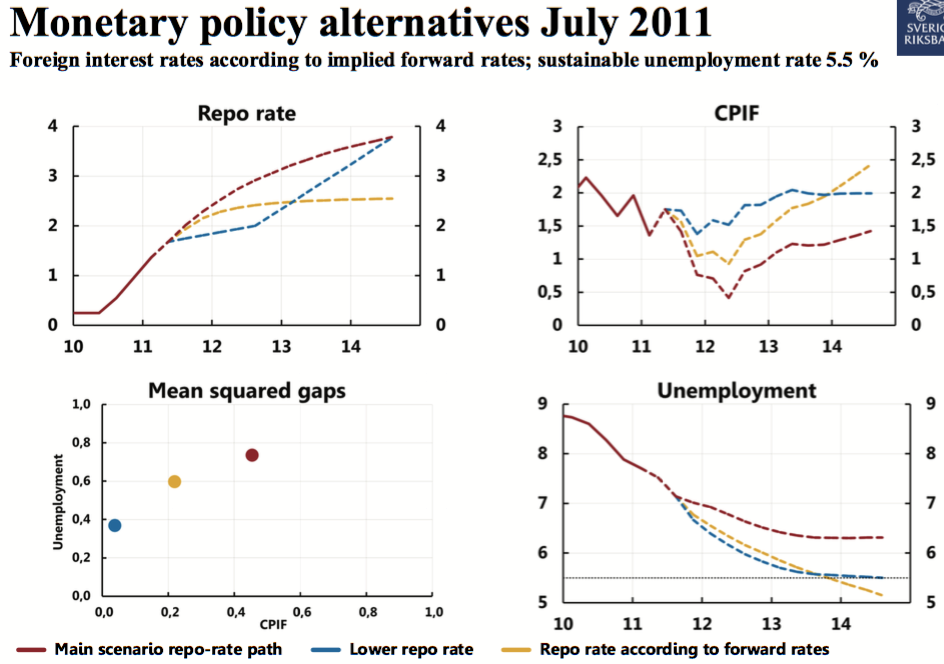

Figure 1. Policy alternatives in April 2011

Figure 1 is the original for figure 2 in the April 2011 minutes. Panel (a) shows two policy-rate paths. The red dashed line is the majority’s path; the blue dashed line is the minority’s path, the one I voted for. Panel (c) shows the corresponding CPIF inflation forecasts. Panel (d) shows the corresponding unemployment forecast for two alternative assumptions about the long-run sustainable unemployment rate, 5.5 percent and 6 percent. I will use 5,5 percent (the red and blue dashed lines), which as explained in the minutes was my estimate at the time.

Panel (b) shows the corresponding mean squared gaps (the mean squared deviations of the inflation forecast from the inflation target and of the unemployment forecast from its long-run sustainable rate, see for instance this speech). A smaller mean squared gap corresponds to better target achievement.

Starting from the majority policy-rate path in panel (a), we see from the red dashed lines in panels (c) and (d) that the corresponding inflation forecast is below the target and the corresponding unemployment forecast is above the long-run sustainable rate. Thus, according to the policy rule, the policy rate and the policy-rate path should be shifted down one step.

The minority path is a shift down on average and substantially more expansionary

Is the minority’s path, the blue dashed line in panel a, a shift down from the majority’s path? Yes, undoubtedly it is a shift down on average. The important property of the minority’s path is, rather than its precise shape, of course that it corresponds to a more expansionary policy stance in April 2011 than the majority’s path. As explained here, the policy stance of a policy-rate path is in this context best measured by the average policy rate during the forecast period. The average policy rate of the majority’s path is about 0.3 percentage point lower than that of the majority’s path. A three-year lower average of 0.3 percentage point is actually quite a bit more expansionary. Translated into a 4-quarter equivalent, it corresponds to a policy rate that is 0.9 percentage point lower for the first four quarters. This is illustrated as the green dashed line in figure 2, which has the same average policy rate as the blue dashed line. Thus, the minority path is significantly more expansionary than the minority path.

Figure 2. The majority’s policy-rate path (red), the minority’s path (blue) and the 4-quarter equivalent of the minority’s path (green)

The minority path leads trivially to a higher policy rate at the end of the forecast horizon

Obviously, the minority path is not a shift down at the end of the forecast period, in early 2014; there the minority’s path is higher, 3.9 percent, about 0.2 percent higher than the majority’s path. Why is that? Is that a problem, as King indicated?

The policy rate at the end of the forecast period should correspond to the inflation and unemployment forecasts at the end of the forecast period (not at the beginning of the forecast period, as Mervyn might have implied). From panels (c) and (d) in figure 1 we see that, for the minority’s policy-rate path, at the end of the forecast period the forecast for inflation is higher and the unemployment forecast is lower than for the majority’s path. This justifies a higher policy rate at the end of the forecast period for the minority path. Furthermore, because at the end of the forecast period the inflation forecast is close to the target and the unemployment forecast is close to the long-run sustainable rate (and would remain so if the forecast horizon was extended), a policy rate close to the neutral policy rate is appropriate. In April 2011, the assumed long-run neutral policy rate was 4 percent.

In general, with initially an inflation forecast below the target and an unemployment forecast above a long-run sustainable rate, an expansionary on-average shift down of the policy rate would mean that the new inflation forecast would rise more rapidly toward the target and the new unemployment forecast would fall more rapidly toward the long-run sustainable rate. This in turn meaning that the inflation target, the long-run sustainable unemployment rate, and an appropriate policy rate equal to the neutral policy rate would be reached earlier. The lower policy-rate path would therefore normally be steeper for two reasons: First, it would rise from a lower level to the same neutral policy rate. Second, it would reach that neutral policy rate sooner.

Thus, the “lower policy rate and policy-rate path” and the “shift down” should not be understood as a mechanical parallel shift down of the path. First, it should be interpreted as an on-average shift down. Second, it would normally involve a shift down to a steeper policy rate path, reaching the long-run neutral policy rate earlier. These are precisely the properties of the minority path in April 2011.

It also follows that more expansionary monetary policy, if not lowering policy rates, trivially has an element of postponing policy-rate increases. Later on, it normally results in increasing the policy rate earlier rather than later.

The minority path was only the first step towards an appropriate and well-balanced policy

Furthermore, from panels (c) and (d) we see that, for the minority path, the inflation forecast was very close to the target whereas the unemployment forecast started far above the long-run sustainable rate of 5,5 percent and ended slightly below the long-run sustainable rate. In that situation, since unemployment deviated more from the long-run sustainable rate than inflation deviated from the inflation target it is clear that a larger shift down of the minority path would bring better target achievement. Thus, more than one step would be needed to get to a well-balance policy, and the minority’s April 2011 policy-rate path was only the first step, not the only step, towards a well-balanced policy.

This is supported by the situation in the next meeting, in July 2011. In figure 3, the original for figure 4 in the July 2011 minutes, the northwest panel shows the minority’s path shifted down further from majority’s path than in April 2011, whereas the right panels show an inflation forecast on average below the target and an unemployment forecast on average above the long-run sustainable rate. This shows that an even lower policy-rate path than the minority’s would bring better target achievement.

Figure 3. Policy alternatives in July 2011

The mean squared gaps in both figures 1 and 3 show that the minority’s path implies better target achievement (lower mean squared gaps) for both inflation and unemployment than the red path. In each case, at the next meeting, another step in an expansionary direction would further improve target achievement. Eventually, after several steps and meetings, the dots corresponding to alternative policy-rate paths would line up in a northwest-southeast direction instead of a southwest-northeast direction, showing that there is a tradeoff between stabilizing inflation around the inflation target and stabilizing unemployment around its long-run sustainable rate and indicating that policy is getting close or equal to a well-balanced policy (this is explained in this speech).

This means that, for the majority’s path to be close to an appropriate and well-balanced policy, the dots showing mean squared gaps for alternative lower or higher policy-rate paths should line up northwest and southeast of the dot corresponding to the majority’s path. That the dots for lower policy-rates paths instead lie southwest of the dot for the majority’s path, instead shows that the majority path is far from an appropriate and well-balanced policy and that several moderate steps down are needed to reach such a policy.

The mean squared gaps in both figures 1 and 3 show that the minority’s path implies better target achievement (lower mean squared gaps) for both inflation and unemployment than the red path. In each case, at the next meeting, another step in an expansionary direction would further improve target achievement. Eventually, after several steps and meetings, the dots corresponding to alternative policy-rate paths would line up in a northwest-southeast direction instead of a southwest-northeast direction, showing that there is a tradeoff between stabilizing inflation around the inflation target and stabilizing unemployment around its long-run sustainable rate and indicating that policy is getting close or equal to a well-balanced policy.

In summary

In summary, counter to the impression King tried to give, the minority’s policy rate and path were fully consistent with the policy rule I followed, several steps down of the policy-rate path would be needed to reach an appropriate and well-balanced policy, and the majority’s policy was not broadly accepted by all members.

Se more about the Goodfriend and King review here, here, and here.

(This post was substantially revised and updated on May 15, 2016.)