English translation of Ekonomistas post.

An odd thing is the Riksbank’s repeated assertions, if not nagging, about how expansionary the Riksbank’s monetary policy is supposed to be. “A very expansionary monetary policy,” it says in the Monetary Policy Update December 2014, and so said the Governor Ingves at the press conference after the policy announcement. But according to what criterion would monetary policy be expansionary? According to standard criteria, including comparisons with other countries, the Riksbank’s monetary policy is by no means expansionary, but by all accounts quite contractionary. One may ask whether the Riksbank’s repeated assertions are due to ignorance or is an example of disinformation.

Comparison with other economies

The policy rate is zero, and among the lowest in the world, as shown in figures 1 and 2.

Figure 1. The policy rate in Sweden, the UK, and the US; the eonia rate in the euro area. Source: Datastream.

Figure 2. The policy rate in Sweden, Canada, and Norway. Source: Datastream.

But the nominal policy rate is not a good measure of the stance of monetary policy. The real policy rate, the policy rate minus actual inflation, is a better measure. (This means assuming that expectations of inflation over a short period is given by average actual inflation during the last 12 months; not an unrealistic assumption, I believe.)

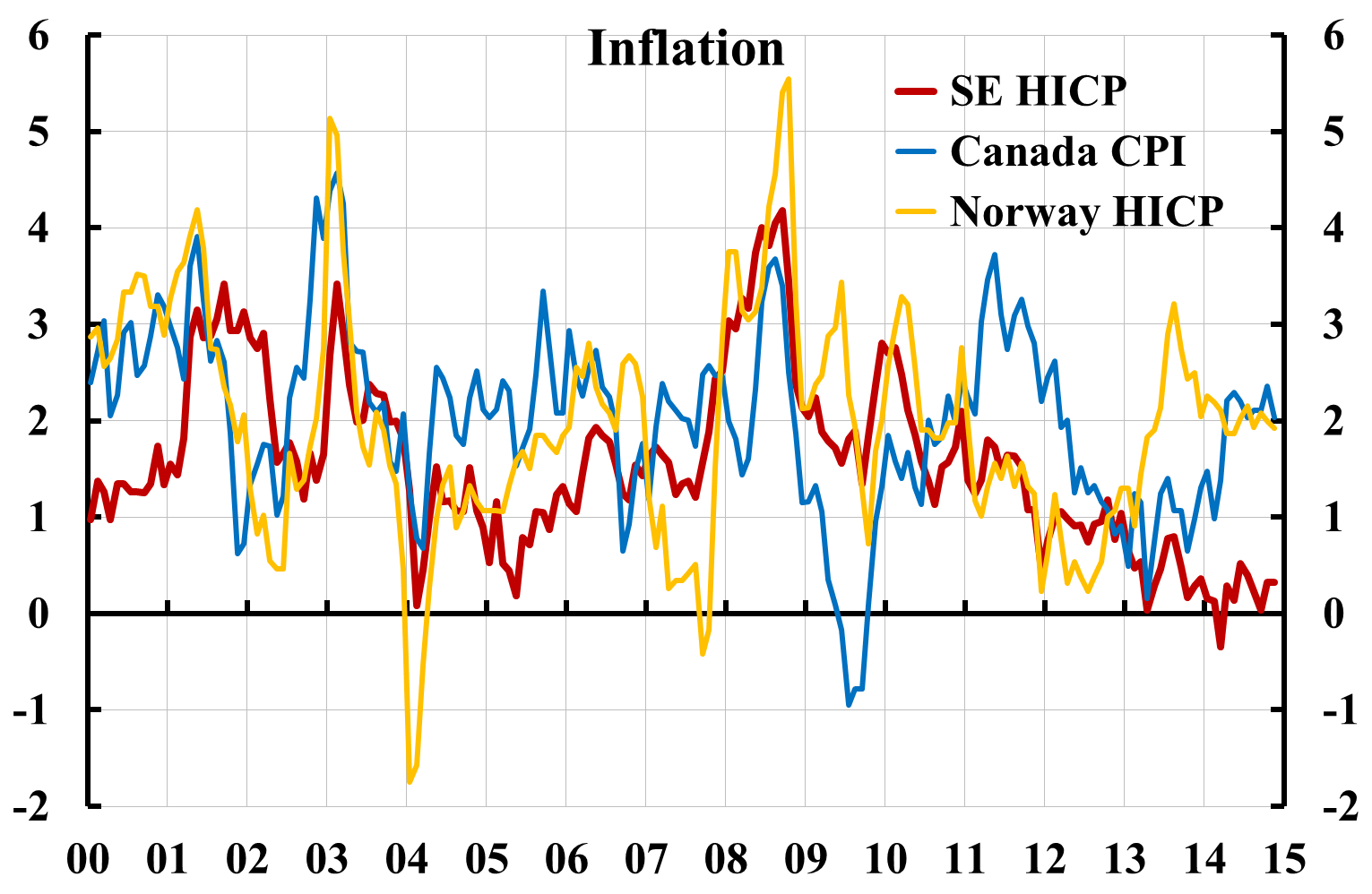

Inflation in Sweden is significantly lower than in other economies except the the euro area, see figures 3 and 4. (To be better internationally comparable, it is measured by the HICP for all economies except the US and Canada, where it is measured by the core PCE deflator and the CPI, respectively. See more discussion in this earlier post.)

Figure 3. Inflation measured by the HICP in Sweden, the euro area, and the UK, and measured by the core PCE deflator in the US. Source: Datastream.

Figure 4. Inflation measured by the HICP in Sweden and Norway and by the CPI in Canada. Source: Datastream.

The fact that inflation is significantly lower in Sweden means that the real policy rate in Sweden is higher than in the other economies (except recently in the euro area and the UK), see figures 5 and 6.

Figure 5. The real policy rate in Sweden, the UK, and the US; the real eonia rate in the euro area. Source: Datastream.

Figure 6. The real policy rate in Sweden, Canada, and Norway. Source: Datastream.

Since inflation and a reasonable inflation forecast is lower in Sweden than for the other economies in the figures (except perhaps for the euro area), and the unemployment rate and a reasonable forecast for unemployment is higher than in other comparable countries, the real policy rate should be lower in Sweden than in the other economies. But it is actually higher than the real policy rates in Canada, Norway, and the United States, despite higher inflation and lower unemployment in these countries. Having previously been much higher than in the Eurozone and the UK, the real policy rate in Sweden is now at about the same level as the real interest rate in those economies (even though unemployment in the UK is falling and is much lower than in Sweden). In comparison with these economies the Riksbank’s monetary policy is not at all expansionary.

Comparison with the neutral real interest rate

The best measure of the monetary policy stance, however, is what one can call the policy-rate gap, the gap between the real policy rate and the neutral real interest rate. Monetary policy is expansionary, neutral, or contractionary depending on whether the policy-rate gap is negative, zero, or positive, respectively.

The neutral real interest rate varies over time and with the state of the economy, is not directly observable, and must be estimated with various methods. There is currently no established estimate of the neutral real interest rate in Sweden. The Riksbank has recently published an Economic Commentary where possible reasons for the neutral real interest rate in Sweden being low for a long time are discussed, but no numerical estimates are presented. In an Ekonomistas post (in Swedish), Henrik Erikson concluded that the neutral real interest rate in Sweden would now be about minus 0.25 percent. This means that the policy-rate gap for this measure of the neutral real interest rate is approximately zero, that is, that monetary policy would be roughly neutral, not expansionary. Erikson’s neutral real interest rate is a slightly longer neutral rate, the 5-year real interest rate expected by the market in 5 years.

A specific definition of a more short-term neutral real interest rate is the real policy rate that would be required to bring the unemployment rate in 1-2 years to a long-run sustainable rate. Obviously, there is uncertainty about what the long-run sustainable rate is – see the discussion in my recent report “Monetary policy and full employment” (in Swedish). Pending better estimates, my preliminary view has so far been that the long-run sustainable unemployment rate may be around 5.5 percent (the midpoint 6.25 percent of the Riksbank’s estimated interval for the long-run sustainable unemployment rate, minus a bias of 0.75 percentage points due to the average historical unemployment rate being higher because of average inflation being lower than average inflation expectations). Even if one were to accept the Riksbank’s estimate of 6.25 percent, it is reasonable that the real policy rate would have to be several percentage points below zero, perhaps minus 3 percent or even lower still, for the unemployment rate to come down to such rates within 1-2 years. According to the NIER forecast in the The Swedish Economy December 2014, which is conditional on a much lower policy-rate path than the Riksbank’s path in the Monetary Policy Update December 2014, the unemployment rate would be as high as 7.8 percent in the first and second quarters of 2016. A significantly lower real policy rate would be needed to get down to around 6 percent. Some rough calculations I have made with the Riksbank’s model Ramses suggests that a real policy rate of minus 3 percent or even lower would be needed.

By comparison, it can be noted that Sweden had a real policy rate of minus 2.5 per cent in early 2010, and that Britain, because of high inflation, had a real policy rate of approximately minus 4 percent in 2011, as is shown in figures 3 and 5 . This also demonstrates how important it is to keep inflation up, in order to, if necessary, be able to have a negative real policy rate despite the lower bound of the policy rate. Had the Riksbank not hiked the policy rate in 2010-2011, inflation would now have been significantly higher, and the possibility of having a negative real policy rate would have been much better, as my counterfactual experiments shows. Figures 5 and 6 furthermore show the large and unprecedented tightening of the Riksbank’s monetary policy that took place in 2010-2011, when the real policy rate increased by a full 3.5 percentage points, from minus 2.5 percent to plus 1 percent.

Compared with a neutral real interest rate of minus 3 percent or more, the policy-rate gap is thus positive and several percentage points large. According to this, the Riksbank’s monetary policy is very contractionary. That monetary policy is contractionary is also apparent in that the NIER’s inflation forecast, despite being conditional on a much lower policy-rate path than the Riksbank, is for several years far below the target and its unemployment forecast is high above a reasonable long-run sustainable rate.

The Riksbank needs to do more

This means that the Riksbank urgently needs to do much more, to bring inflation up to the inflation target and unemployment down towards a long-run sustainable rate. The policy rate should already have been reduced to minus 0.25 percent. It is possible that it may even be possible to set it at minus 0.5 percent. Quantitative easing, that is, asset purchases, may further drive down long-term rates somewhat. A currency depreciation and an exchang-rate floor, in line with what the Czech National Bank has done and what is discussed in this post, would probably be the most effective action. There is no reason not to take these actions together, in the hope that the total effect will be sufficient. In this situation, decisiveness, not indecision, is what is required.

Ignorance or disinformation?

In light of the above, it is odd that the Riksbank reiterates its claims that the Riksbank’s monetary policy would be very expansionary. Is the Riksbank’s Executive Board so ignorant of these common and sound measures of the monetary policy stance, or do we see an example of disinformation from the Riksbank?