[English translation of new Ekonomistas post.]

IMF’s annual so-called Article IV report on Sweden is now available on IMF’s web site. I have previously noted that the IMF mission’s concluding statement in June was partial and biased. The final report continues in the same vein. Given that the report to a large extent deals with household debt, it is particularly remarkable that it contains crucial factual errors about household debt and misleading information about housing prices. It gives the definite impression of having been guided by preconceptions rather than facts and analysis.

For instance, the report states that

”Housing prices and household indebtedness have increased from already high levels.” (p 5)

”Household debt ratios have continued to rise and remain particularly high among lower-income households.” (p 6)

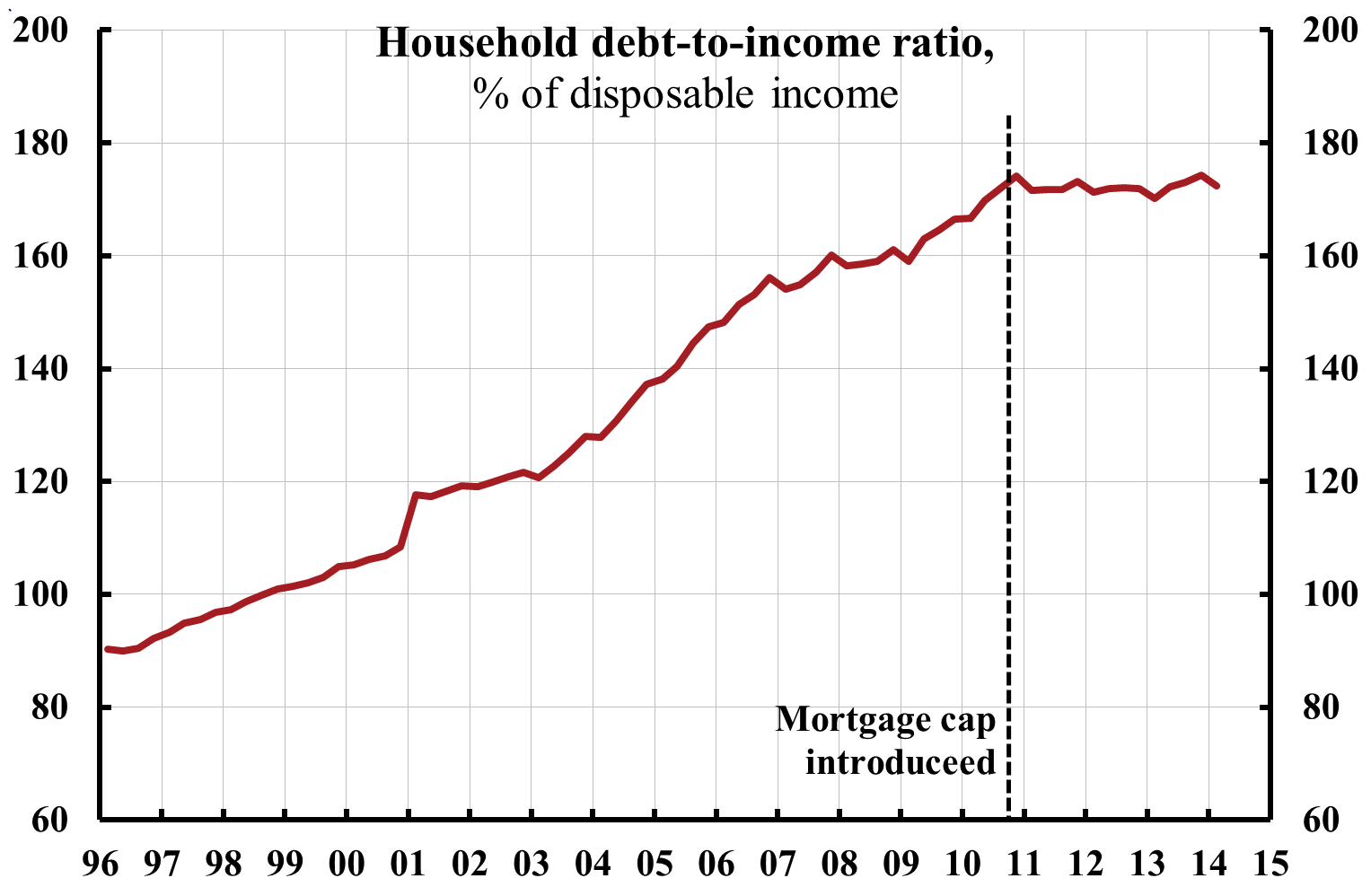

The household debt ratio has NOT increased since the fall 2010

Has “household debt ratios continued to rise”? No, the household debt ratio has NOT increased since the fall 2010, when Finansinspektionen (the Swedish FSA) introduced a mortgage cap of 85 percent. As is shown in figure 1, in the first quarter of 2014 the debt ratio was at exactly the same level, 172 percent, as in the third quarter of 2010. This has been discussed in this previous post.

Figure 1. Household debt as a percentage of disposable income.

Source: Statistics Sweden

The debt ratio is NOT particularly high among lower-income households

Are household debt ratios “particularly high among lower-income households”? No, the debt ratios are NOT particularly high among lower-income households.

As is discussed in detail in a previous post, according to a Riksbank study, indebted lower-income households have about the same debt ratio, about 250 percent, as other households (see this figure, where one, however, has to disregard the first decile, which is problematic and difficult to interpret – with some households with negative income and large debt, and probably a few well-off people with zero taxable income because of large deductions). But the share of debt-free lower-income households is, according to a Government Commission of Inquiry by Anna Hedborg, much higher for lower-income households than for higher-income households (see this table). In the three bottom income groups, about 50 percent or more of the individuals are without debt, whereas in the three top income groups, only about 20 percent are without debt.

Thus, higher-income households are indebted to a substantially larger extent than lower-income households. Higher-income households also have large debts to a higher extent. The aggregate debt ratio (including both indebted and debt-free households) is thus substantially lower for lower-income households (see this figure).

Housing prices have on average increased LESS than disposable income since 2007

Have housing prices “increased from already high levels”? Since disposable income in current prices has increased, one can hardly expect housing prices in current prices to fall during a longer period. If this were the case, as a share of disposable income, housing costs at unchanged mortgage rates would fall over time, which is hardly realistic. Therefore, to start with, it is reasonable to relate the growth of housing prices to the growth of disposable income.

As can be seen in figure 2, aggregate housing prices have on average increased LESS than disposable income since 2007. Relative to disposable income, aggregate housing prices were in the spring 2014 about 7 percent lower than in August 2007. Prices of flats (owner-occupied cooperative housing) have increased faster than (owner-occupied) houses and have now compared to August 2007 increased somewhat more than disposable income. Prices of houses have increased less, and, since the housing stock to a larger extent consists of houses than flats, aggregate housing prices have increased less than disposable income. This is discussed in this previous post.

It is not wrong to say that housing prices have increased, but it is very misleading not to compare with the increase in disposable income.

Figure 2. Housing prices and disposable income in current prices. Index August 2007 = 100.

Source: Statistics Sweden and Valueguard.

As said above, the IMF mission’s concluding statement in June was partial and biased, which I have previously shown in detail. The final report continues in the same vein. It gives the definite impression of having been guided by preconceptions rather than facts and analysis. It does not deserve to be taken seriously.