[English translation of new Economistas post (in Swedish).]

The household debt ratio – household debt as a percentage of disposable income – is an unsuitable risk measure and there are much better ones. In spite of this, the Riksbank and others attach large weight to how the debt ratio develops. For those who consider the debt ratio a relevant risk measure, it should be somewhat comforting that the debt ratio fell somewhat in the first quarter of 2014, in contrast to some alarmist warnings about rapidly increasing debt.

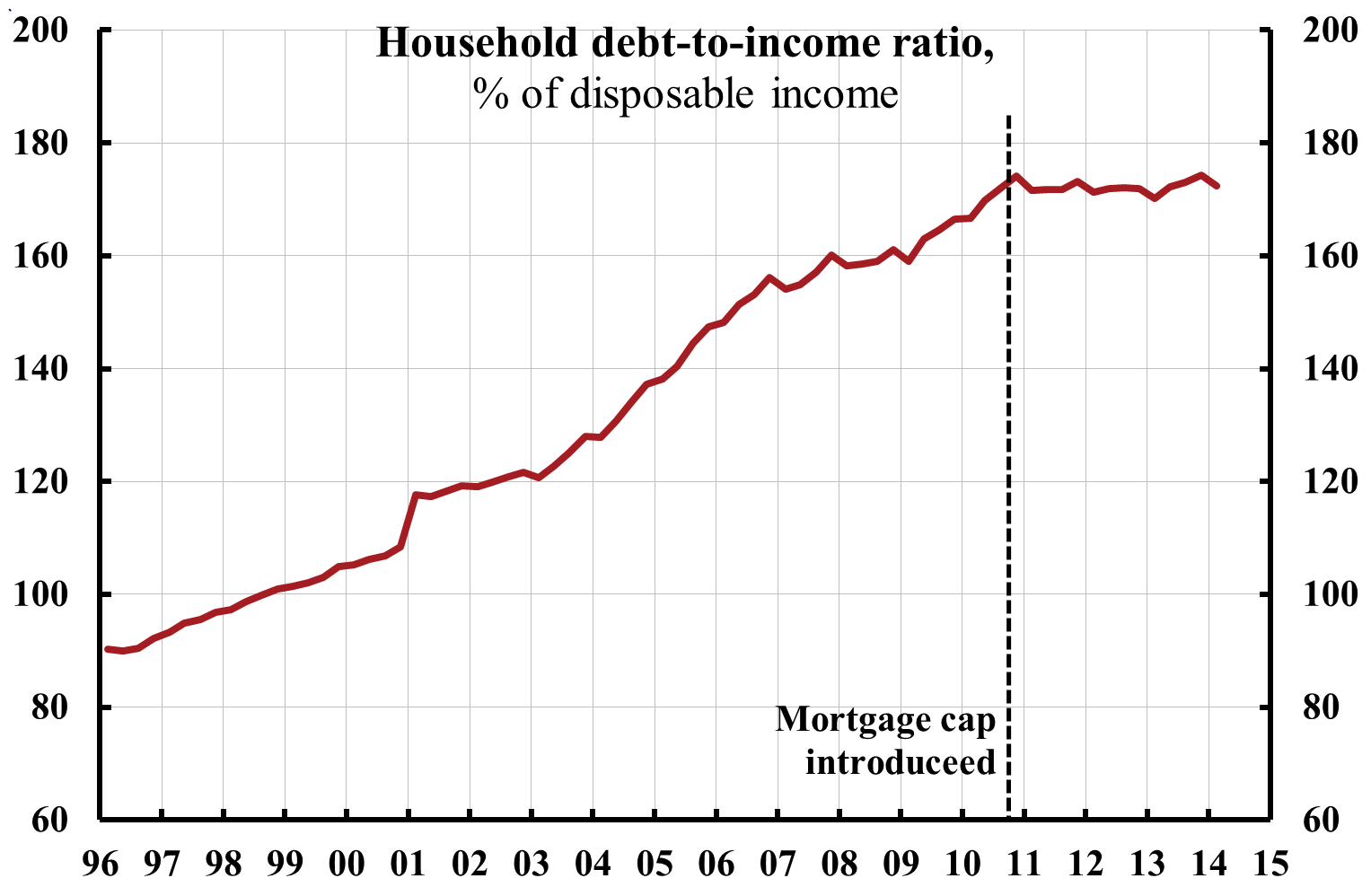

The debt ratio fell from 174 percent for the fourth quarter of 2013 to 172 percent for the first quarter of 2014. [1] The debt ratio is now at precisely the same level as in the fall of 2010. It has been quite stable around that rate since Finansinspektionen (the Swedish FSA) introduced a mortgage cap in October 2010. Thus, since then household debt has increased at the same rate as disposable income.

Figure 1 shows a time series of the debt ratio since 1996. It increased from the middle of the 1990’s to the fall of 2010 for several reasons discussed in this memo of Sten Hansen and this report from the consulting company Evidens (both in Swedish only). (The two largest causes of the increase in the debt ratio are a rise in the share of households that own rather than rent their housing and a fall in the effective taxation of housing; lower mortgage rates are only in third place.) Since the fall of 2010, the debt ratio has stabilized around 172 percent.

Figure 1. Household debt as a percentage of disposable income.

Source: Statistics Sweden.

Figure 2 shows time series of household debt, disposable income, and debt ratio, all indexed to 100 in the third quarter of 2010. We see that household debt grew faster than disposable income up to the fall of 2010, but that debt and disposable income thereafter have grown at the same rate.

Figure 2. Houshold debt, disposable income, and debt ratio (index 2010q3 = 100)

Source: Statistics Sweden.

How have housing prices developed over time relative to disposable income? In contrast to some alarmist warnings about rapidly growing housing prices, these have on average grown at a somewhat slower rate since the fall of 2007, see this post and figure 3.

Figure 3. Nominal housing prices and household disposable income.

Source: Statistics Sweden and Valueguard.

[1] The debt ratio is calculated from total household debt reported in the Financial Accounts of Statistics Sweden (published June 18 for the first quarter 2014) and from household disposable income during four quarters, reported in the National Accounts of Statistics Sweden (published May 30 for the first quarter 2014). Back to text.