New Ekonomistas post (in Swedish). Here is an English translation.

The Riksbank tries, in a box in its latest Monetary Policy Report, to counter my research and my posts about the effect of monetary policy on household indebtedness. The Riksbank tries to show that the effect of a lower policy rate is to increase real debt and the debt ratio, not to decrease them, as I have maintained. It is of course positive that the Riksbank engages in a discussion of these matters and tries to justify its policy better. But the Riksbank’s estimated effect turns out to be very small and not economically significant. And with a considerable margin, it is not statistically significant. In addition, the econometric model used in the estimation is not correctly specified. The Riksbank’s box thus has little weight, and it provides no support for the Riksbank’s policy.

“Leaning against the wind” means a tighter policy than is justified by stabilizing inflation around the inflation target and unemployment around a long-run sustainable rate. The Riksbank pursues such a policy in an attempt to limit any risks associated with household debt. I have maintained that “leaning against the wind” is a very unsuitable, and even counterproductive, way to try to reduce any such risks. I have used two arguments.

The first argument is under the assumption of rational expectations and is developed mainly in this paper and discussed in this post. There I have shown that a tighter policy normally has too little effect on household debt in relation to the effect on unemployment and inflation to be justified. The effect may even go in the wrong direction, in the sense that a tighter policy leads to higher real debt and debt-to-income ratio (but the effect is still too small to have any impact on any risks). This is due to a higher policy rate probably reducing the price level, nominal GDP, and nominal disposable income faster than total nominal debt.

The second argument relies on the fact that the tight monetary policy has led to actual inflation being much loser than expected by Swedish household. Then monetary policy has a substantial effect and substantially increase real debt and the debt ratio. An actual inflation rate of zero during the last two years has led to about 4 percent higher real debt compared to if inflation had equaled the inflation target of 2 percent. This is discussed most recently in this post.

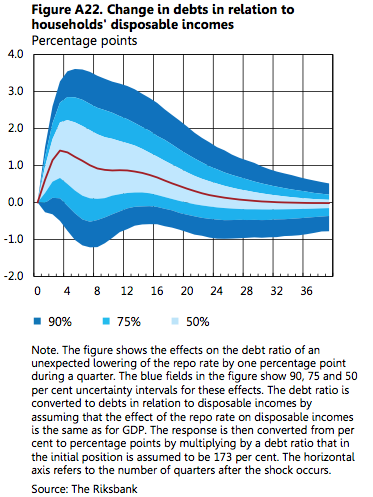

The Riksbank now tries to contradict the first argument, by reporting the result of an empirical estimation with a so-called vector auto regression (VAR). According to this estimation, a lower policy rate, about 1 percentage point lower for 4 quarters, leads to an increased real debt and debt ratio. This implies that a higher policy rate would lead to lower real debt and debt ratio, counter to my first argument above.

The effect is small an neither economically and significantly larger than zero

The first thing one notes is that the Riksbank’s estimate of the effect is small. As we see in figure A22, the increase in the debt ratio is 1.4 percentage points. That is, an increase from the starting point of 173 percent of disposable income to 174.4. Expressed in percentage change, it is an increase of 1.4/173 = 0.8 percent. Such a small increase has no noticeable impact on any risks associated with the debt. The increase is thus not economically significant.

Neither is it statistically significant. That is, the hypothesis that effect is zero or negative cannot be rejected at a reasonable significance level. As we can see in figure A22, the 90-percent uncertainty interval does not lie above zero. This means that the hypothesis that the effect is zero or negative cannot be rejected at a 5 percent significance level. [1] Neither does the 75-percent uncertainty interval lie above zero. This means that the hypothesis that the effect is zero or negative cannot be rejected even at a 12.5 percent significance level. One can thus not exclude that the effect is negative. The 50-percent uncertainty interval is barely above zero for quarter 8. This means that hypothesis that the effect is zero or negative can be rejected only at a high significance level of 25 percent. For a result to be considered statistically significant, the significance level should normally be at most 5 percent.

Thus, the increase is very small and neither economically nor statistically significantly greater than zero. One cannot exclude that the debt ratio would fall somewhat rather than increase. The Riksbank should thus draw the conclusion that the policy has a very small effect on the debt ration, neither economically nor statistically significant. The Riksbank’s box does thus not give any support whatsoever to its monetary policy.

The Riksbank’s econometric model is misspecified

To this can be added that the Riksbank’s econometric VAR model is misspecified. First, in order to correctly estimate the empirical effect of the policy rate on debt, one must control for other factors affecting debt. According to table 1 (page 2) in an excellent memo by Sten Hansen (unfortunately only available in Swedish) to the Council for Cooperation on Macroprudential Policy, the most important factors behind the change in Swedish household’s debt-to-income ratio is a higher share of housing owned and lower taxes on housing. Together they may have had a four times as large impact as lower mortgage rates. In addition, according to Hansen’s memo, there are additional factors besides a higher share of housing owned (page 7, translated from Swedish by me): “First, there has been a fast urbanization process, so much of the newly produced housing is in metropolitan areas which are more expensive than the Swedish average. Second, much rental housing has been converted into cooperative housing, also mostly in metropolitan areas, where housing is more expensive than average. Third, new ownership of housing is associated with an initial high indebtedness, which by itself may imply a somewhat lower future growth rate of the aggregate debt ratio.” If one does not control for these effects, and the corresponding variables are not included in the VAR model, the effects attributed to the policy rate will be misleading.

Second, correctly specified VAR model of mortgages and the policy rate must take into account that mortgages are nominal, not real. It must also take into account that mortgages have an average loan length of several years (on average about 7 years, according to information I have received from some of the banks). This means that only a fraction of the mortgage stock is turned over each year. The VAR model must then have equations that are consistent with these circumstances, in order for the estimate to be meaningful. Since the VAR model used does not fulfill these conditions (for instance, it is expressed in terms of real debt instead of nominal), it is misspecified, and its results are not meaningful.

The more important second argument. about the impact of real debt of an unexpected low price level, is not addressed

Strangely enough, the Riksbank does not try to counter my second argument. That argument is substantially more important, since it concerns substantially larger and economically significant effects. The Riksbank’s monetary policy has resulted in the price level being 4 percent lower than expected by the households. This means that the households’ real debt has become 4 percent higher than if inflation had equaled the 2 percent inflation target. This is a large negative compulsory amortization, of about SEK 40 000 for each borrowed SEK 1 million, see this post. This large effect swamps the small and not significant effects the Riksbank discusses in the box.

[1] The probability of the estimated effect falling outside the 90-percent uncertainty interval is 10 percent, with a 5 percent probability of the effect falling above the uncertainty interval and a 5 percent probability of the effect falling below the uncertainty interval. If the uncertainty interval had been everywhere above zero, the probability that the effect falling on zero or below would have been less than 5 percent. Then one says that the hypothesis that the effect is zero or below can be rejected at a 5 percent significance level, equivalently that the effect is significantly above zero at a significance level of 5 percent.